If you're on an income-driven repayment (IDR) plan for your student loans, you might benefit from using alternative documentation of your income when it’s time to recertify. IDR plans require you to update your income and family size yearly, usually using your most recent federal income tax return. But life can throw curveballs, and your tax return might not always paint an accurate picture of your current financial situation.

In this article, I'll explain alternative documentation of income, when you might need it, and how it can potentially lower your monthly student loan payments.

What is alternative documentation of income?

Alternative documentation of income (ADOI) is any proof of income you provide other than your most recent federal tax return when applying for or recertifying an income-driven repayment plan. This may include:

- W2

- Pay stubs

- Letters from your employer stating your income

- Bank account statements

- Interest or dividend statements

- A signed statement explaining your income sources

Keep in mind that you might also need to submit proof of your spouse’s taxable income, depending on your situation. This is why talking to a student loan professional is so important. The lower your reported income, the lower your student loan payment, so you don’t want to include your spouse’s income if you don’t have to.

Why is it considered “alternative” documentation?

Studentaid.gov recommends using the IRS Data Retrieval Tool (DRT) to automatically import income information for your IDR plan. But your tax return doesn’t always reflect what you’re earning right now. For example, your income might have gone down since filing your last tax return, or maybe you had a one-time event that inflated your taxable income.

In these cases, you can provide “alternative” documentation of your income, such as pay stubs, employer letters, or bank statements. If you initially consented to let the Department of Education access your tax information, your student loan servicer will automatically recertify your plan each year and notify you of any changes to your payment amount.

Even if you opted for automatic annual recertification, you can revoke automatic income sharing access and manually complete the IDR plan request. Manually recertifying with alternative documentation can help lower your monthly payments to better match your current earnings.

When to use alternative documentation of income

Knowing when to use alternative documentation can help keep your federal student loan payments manageable. Here are some common scenarios to consider using it:

- Your income has decreased: If you recently lost your job or are earning less money now than when you last filed taxes, ADOI can help lower your payment.

- Your marital status changed: If you recently divorced or separated and previously filed a joint tax return, your individual income may be different from what was reported on your last tax return.

- You had a one-time income event: If you sold an asset or had another one-time event that’s reflected on your tax return, your earnings may look higher than they really are.

- You live in a community property state: If you file taxes as married filing separately in a community property state, your income is split 50/50 on your federal tax return. If you make less than your spouse, your actual income is lower than what’s shown on your tax return.

Related: Married Filing Separately in Community Property States Due to Student Loans: Complete Guide

Example: Alternative documentation in action

Let’s say you’re on the Saving on a Valuable Education (SAVE) plan and recently lost your job. Importing your previous tax return using the DRT shows an adjusted gross income of $250,000, but now you’re earning only $75,000 from a part-time position. You can recertify your income using your pay stub instead of your last tax return to reflect this change.

Here’s how it works: If your original monthly payment was $1,801 based on the $250,000 income, the lower income of $75,000 will drastically reduce your payment amount. The SAVE plan uses 10% of your discretionary income (income above 225% of the poverty line) to calculate payments.

Assuming a family size of one, 225% of the poverty line is about $33,885. So, your discretionary income is $41,115 ($75,000 – $33,885).

Under the SAVE plan, your new payment would be $343 — $1,458 less than what you were paying.

When not to use ADOI

Using something other than your tax return to certify your income can be really helpful, but it’s important to use it correctly.

Never use ADOI to underreport your income or misrepresent your financial situation. If you do, it could be considered fraud and lead to serious consequences, like losing eligibility for IDR or even facing legal action. Always provide truthful and complete information when documenting your income to avoid any issues.

How to provide alternative documentation of income

If your circumstances have changed since your last federal income tax return (e.g., job loss, drop in income, separation, or divorce), and your income is now lower or your family size has changed, you can recertify your income immediately instead of waiting for the scheduled recertification.

You'll work directly with your loan servicer or recertify your income on the Studentaid.gov website using alternative income documentation instead of the DRT. You’ll need to provide income documentation or attest that you have no taxable income.

Here’s a step-by-step guide to help you recertify your IDR plan:

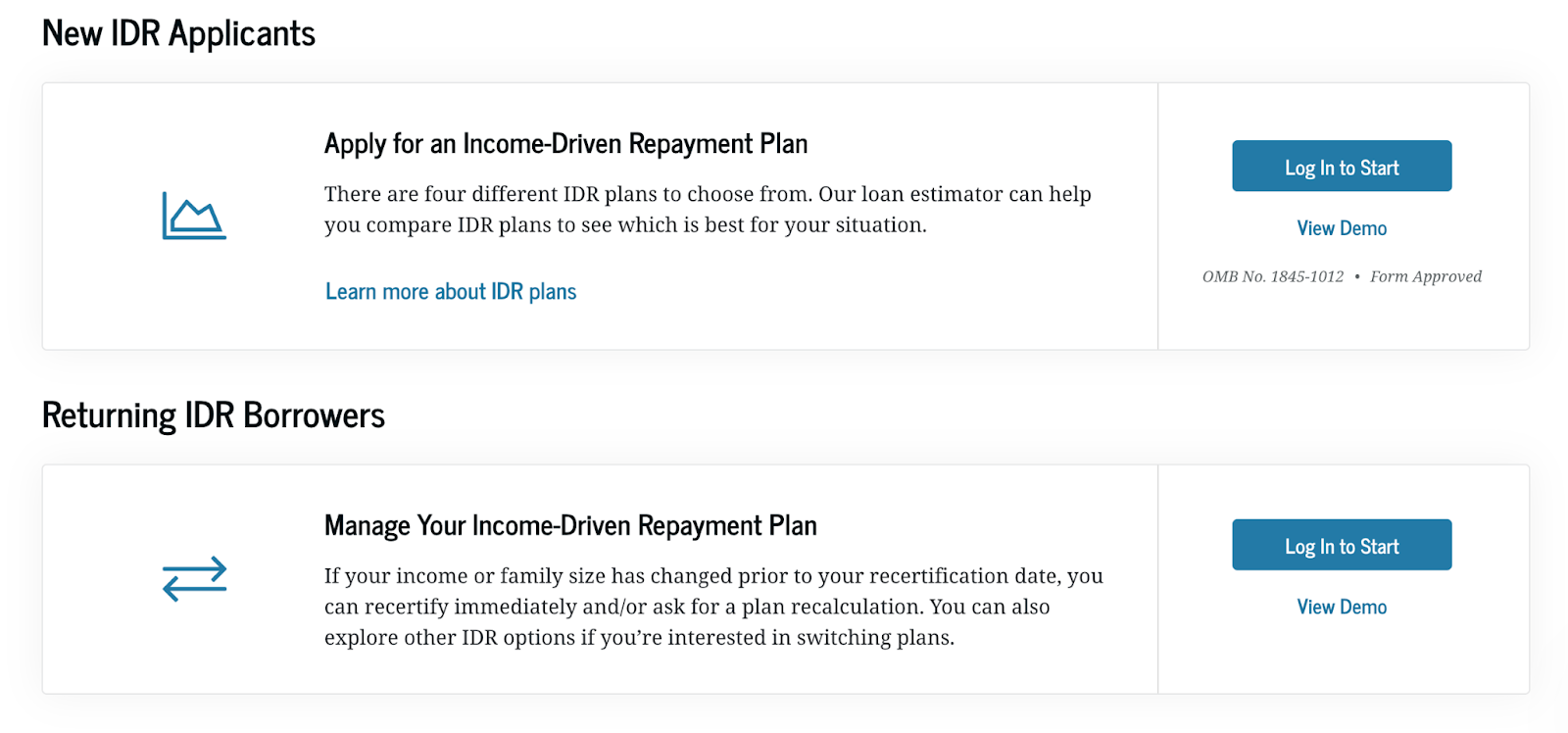

1. Go to the IDR plan request page.

Scroll down to “Returning IDR Borrowers” and click the “Log In to Start” button. You must log in with your Studentaid.gov account username and password (FSA ID).

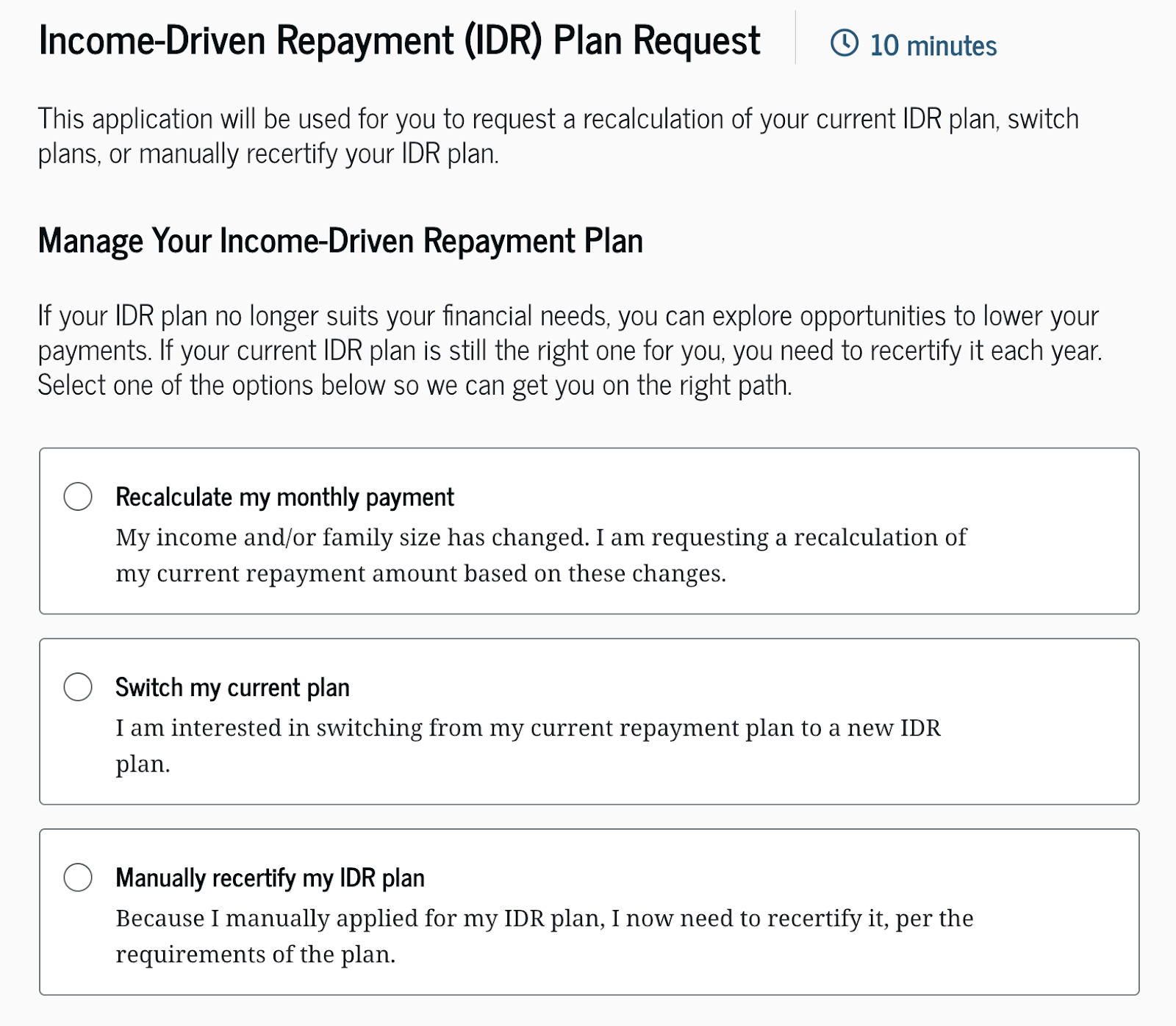

2. Select “Recalculate my monthly payment.

This link is in the “Manage Your Income-Driven Repayment Plan” section.

3. Verify your information.

Review and update your address and contact information, as well as your marital status, family size, dependents and income information.

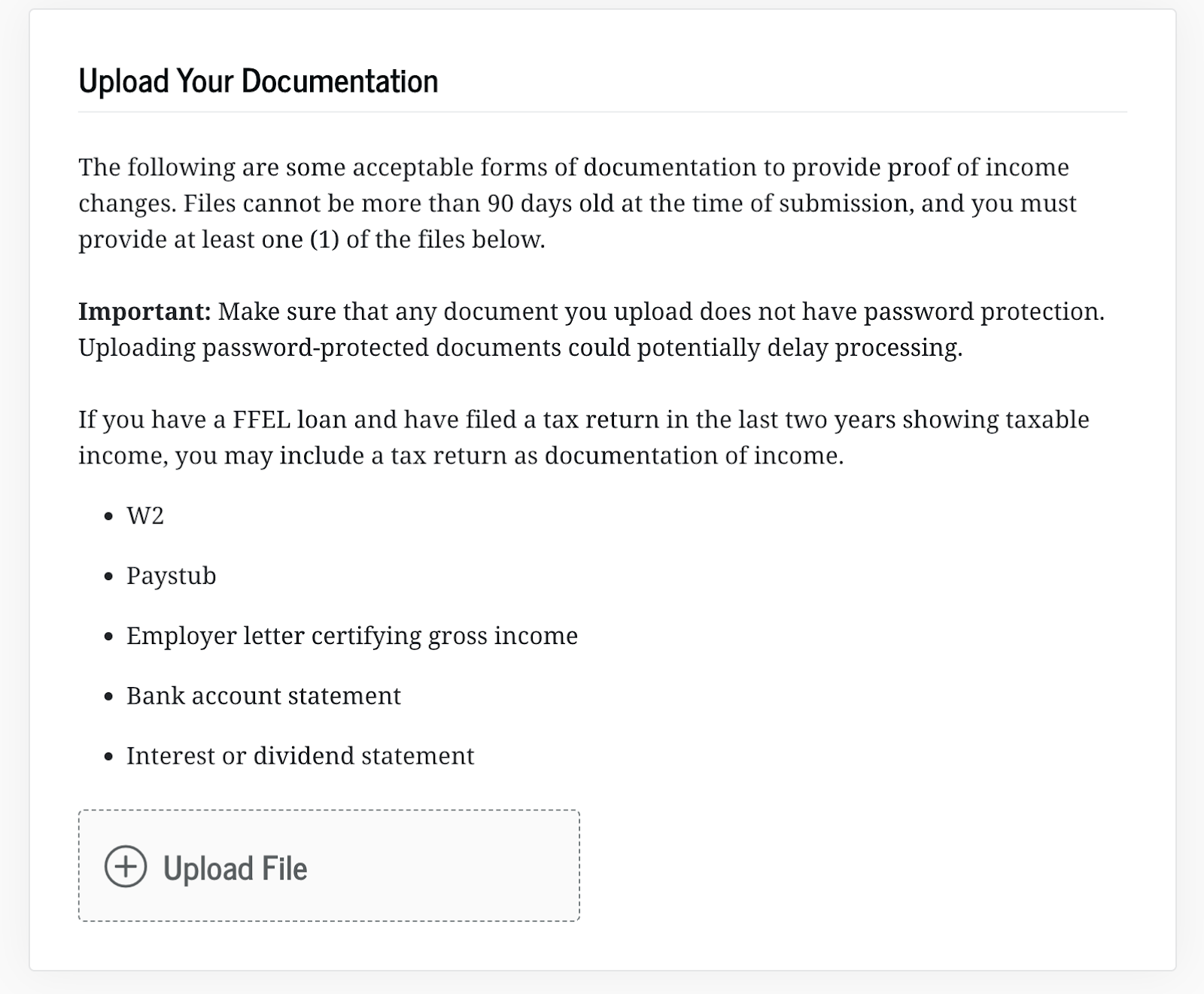

4. Upload documentation.

Click on “Upload File” to provide proof of income changes. When submitting alternative documentation:

- Use recent proof. Any proof you provide must be dated within 90 days of the date you signed your IDR application.

- Include required documents. The Department of Education requires that you submit at least one of the following document types: W2, paystub, employer letter, bank account statement, or interest or dividend statement.

- Label your documents. Before uploading, label each document with your name and student loan account number.

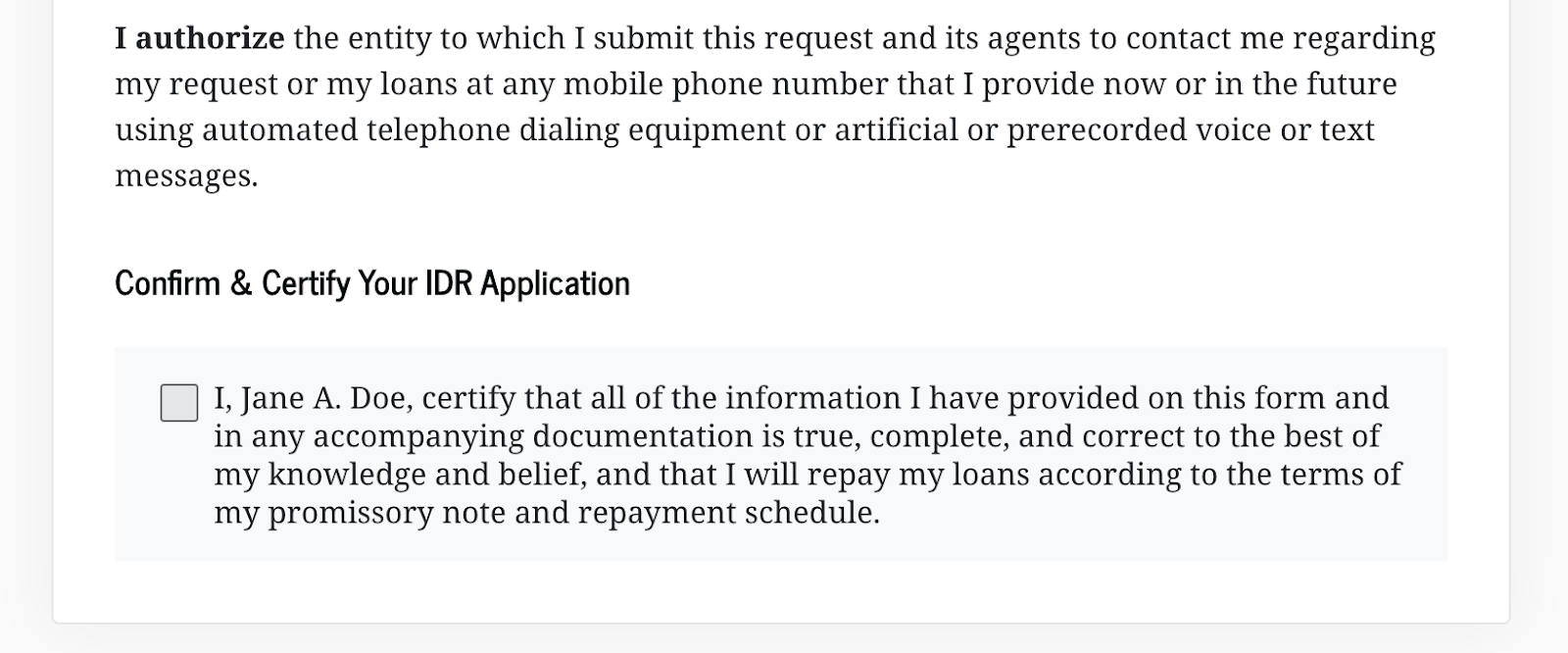

5. Review your application and submit it.

Review the revisions you made to make sure they’re correct. Then, check the box to confirm and certify your IDR application information before submitting the information.

What counts as income for IDR repayment calculations?

The Department of Education is only interested in your taxable income when calculating your IDR payments. Taxable income can come from:

- Employment

- Self-employment

- Business income

- Dividend and interest income

- Tips

- Alimony

You don’t need to report untaxed income such as Supplemental Security Income, child support, or federal or state public assistance.

If you have no income or untaxed income

If you’re not working or only receiving untaxed income, just check the appropriate box on the form. You won’t need to send in any further proof.

What happens if you don’t recertify by the deadline?

It’s very important to recertify your income and family size by your anniversary date, even if your income stays the same. Missing this deadline can have different consequences depending on your plan:

- For the SAVE plan: If you don’t recertify on time, you’ll be removed from the Saving on a Valuable Education (SAVE) plan and placed on an alternative repayment plan. This plan won’t base your payments on your income, which could mean a higher payment amount.

- For other plans (PAYE, IBR, ICR): If you miss the deadline for plans like Pay As You Earn (PAYE), Income-Based Repayment (IBR), or Income Contingent Repayment (ICR), you won’t be removed from your IDR plan. But your monthly payments will switch to what you’d pay under a 10-year Standard Repayment Plan, calculated from your loan balance when you first entered the IDR plan.

In either case, you can get back to making payments based on income by providing your servicer with updated income information, as long as you still qualify.

Maximizing your IDR plan with alternative documentation

Using alternative documentation of income for IDR plans can be a valuable tool for student loan borrowers. It ensures your IDR payment aligns with what you’re actually earning, helping you manage your student loan debt more effectively.

For personalized guidance, book a consultation with me or another student loan planner on our team. We can help you figure out exactly what you need to report to keep your payments as low as possible.

Not sure what to do with your student loans?

Take our 11-question quiz to get a personalized recommendation for 2025 on whether you should pursue PSLF, SAVE or another IDR plan, or refinancing (including the one lender we think could give you the best rate).