Many student loan borrowers worry that the forgiveness programs they counted on during the Biden administration could be going the way of the dodo bird with the potential elimination of the Department of Education.

President Donald Trump has made closing the Department of Education and shifting its functions to individual states a top priority of his administration. The so-called Department of Government Efficiency (DOGE) group, led by Elon Musk, deployed a team to the Department of Education headquarters in early February 2025 to help accomplish that task.

What does this mean for borrowers?

- Should borrowers expect that the Department of Education will close?

- Could Public Service Loan Forgiveness (PSLF) and Income-Driven Repayment (IDR) forgiveness get slow-walked from hollowing out staff positions?

- What can the executive branch do without Congress in this case?

We’ll cover what student loan borrowers should know about the potential elimination or downsizing of the Department of Education.

How much power does President Trump have over education policy?

If something is explicitly in a statute, it can’t be permanently changed by the executive branch forever.

That’s one reason you see a lot of funding freezes, administrative paid leaves or buy-out offers being made to government employees. A lot of what the White House would like to do is blocked by various rules or laws.

When they tried to put a freeze on all federal loans and grants, a court blocked it by puting an injunction on it.

The same applies here — President Trump can’t do whatever he wants with education policy, although he does have enormous power over this area with anything that’s not explicitly written in a statute.

As an example, former President Biden created programs like the IDR Waiver, PSLF Waiver, and Saving on a Valuable Education (SAVE) Plan, extended IDR recertification dates over a dozen times, extended the student loan pause over and over again, and more.

None of those programs are in statute, so they could be rolled back or restricted. But reversing a specific student loan program would take a long time. In many cases, negotiated rulemaking committees need to be assembled, and rules must be published in the federal register.

Many of the more technical policy changes the Biden administration made, such as the IDR Waiver/IDR Account Adjustment, would be so difficult to undo it’s almost impossible to imagine a scenario where that additional payment count credit could be reversed.

So, can President Trump change or reverse any Department of Education policy not specifically outlined by Congress or written out in statute? Yes, but he can’t do it overnight.

And most of the core programs borrowers rely on are protected by law. Let’s see why.

What does the statute say about the Department of Education and student loans?

Can the White House transfer the student loan program to the Treasury Department or another government agency? No.

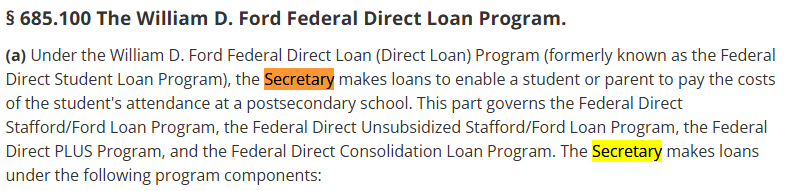

Consider the following from the federal regulations for the student loan program. It’s very explicit that the “Secretary of Education” is responsible for administering the student loan program — no one else.

You might say, “WAIT! It says ‘Secretary,’ not ‘Secretary of Education.’”

But legal definitions confirm that in this context, “Secretary” means the Secretary of Education (source):

That means President Trump cannot relocate the federal student loan system outside the Department of Education, no matter how much he may want to.

What about income driven repayment though?

Related: How and When Student Loan Payments Will Increase Under President Trump

IDR is in the statute and must be provided by the Department of Education

The section on income-driven repayment mentions the Secretary of Education 35 times.

This is where programs like the Income Based Repayment (IBR) program are defined, and it’s explicit about what the rules are.

The only exception is the Income Contingent Repayment (ICR) statute, which doesn’t explicitly confirm forgiveness after “no more than 25 years” — which is why this is a key issue in the ongoing SAVE lawsuit.

PSLF is in the statute and must be provided by the Department of Education

PSLF is also clearly in the statute. The section on PSLF mentions the Secretary of Education 34 times.

So PSLF also has to be provided by the Department of Education — it cannot be outsourced.

Related: Public Service Loan Forgiveness FAQ: 40 Tips to Save Thousands

What could Trump and Musk actually change about the Department of Ed and student loans?

While the Department of Education must continue running student loan programs, any function not explicitly protected by law could eventually be moved or transferred to another department or agency.

A lot of these jobs have nothing to do with student loans.

So, what could President Trump actually change about student loans?

He could:

- Tighten the definition of qualifying employer for PSLF (presumably to what it was before, such as using the “employer definition of full time”).

- Make ICR derived income-driven plans less generous and eliminate SAVE (assuming they’re not blocked outright by a court).

- Audit IDR recertification (imagine a Government Accountability Office-style investigation that probes whether borrowers are not including all sources of taxable income when recertifying, if not using tax returns, which is the safer approach).

- Restrict access to federal student loans (perhaps by limiting access to certain types of schools through a Republican version of a gainful employment rule that targets non-profit universities specifically).

- Freeze hiring at the Department of Education, potentially reducing support for processing forgiveness applications.

- Slow processing of forms and complaints by not providing as many staff members to process them.

This is not an exhaustive list, but notice that repealing PSLF and IDR is not on there. That’s because to actually achieve that, it would take an act of Congress.

But yes, the processing of these programs could potentially become a mess that could last for several months.

Should you worry about the Department of Ed shutting down?

The short answer is no.

There are too many statutory requirements that the Department of Education must do according to law for it to simply disappear.

In reality, the Department of Education is accidentally one of the world’s largest banks.

That, of course, means it will receive a large amount of attention from the White House.

Know that the key programs borrowers are hoping for, such as IBR and PSLF, can’t be permanently blocked no matter how much the White House and DOGE would want to.

Of course, these programs could potentially be reformed, likely for new borrowers only, if Congress were to get involved.

While we know it’s hard, the best thing to do right now is to be patient and know that the first 100 days of any new presidential administration are often filled with head-spinning policy changes. Eventually, a more predictable status quo will settle in on student loan policy.

In the meantime, if you need a plan refresh for your student debt, our experts would love to help.

Refinance student loans, get a bonus in 2026

| Lender Name | Lender | Offer | Learn more |

|---|---|---|---|

|

$1,000 Bonus

Bonus for eligible users who refinance $200k or more. $500 for $100k to $200k (bonus from SLP, not SoFi. Terms apply.)

|

Fixed 3.99 - 9.99% APR

Variable 5.74 - 9.99% APR with all discounts with all discounts |

|

|

$1,500 Bonus

For $200k or more. $1,000 for $100k to $200k. $200 for 50k to $100k

|

Fixed 4.25 - 9.99% APR

Variable 5.73 - 9.99% APR

|

|

|

$1,750 Bonus

For $200k+. $1,250 for $100k to $199k. $350 for $50k to $99k. $100 for $5k to $50k

|

Fixed 3.99 - 10.35% APR

Variable 3.63 - 10.72% APR with autopay with autopay |

Not sure what to do with your student loans?

Take our 11-question quiz to get a personalized recommendation for 2026 on whether you should pursue PSLF, IDR, or refinancing (including the one lender we think could give you the best rate).