Whether you’ve already refinanced your student loans to save money on interest or you’re thinking about it, you might wonder — “How often can you refinance student loans?”

The answer is as many times as you want. You can continue your quest to score the lowest rate possible until all of your debt is gone. Whether refinancing student loans multiple times is a strategy you should do is a different story.

In this guide, we’ll cover some examples of when it makes sense to refinance multiple times, when you should hold off and how to get started.

Can you refinance a refinanced student loan?

Our February 2021 student loan refinancing survey showed that awareness around refinancing multiple times is increasing with 69% of respondents saying that they knew refinancing student loans multiple times was possible. In contrast, our December 2019 refinancing survey found that only 60% of respondents knew they could refinance more than once.

When you refinance a student loan, you take out a new private loan with a specific refinancing lender. That means if you have federal student loans, you forego borrower benefits during repayment, such as forgiveness and income-driven repayment, in exchange for lowering your interest rates. In lowering your interest rate, you can shave off years of repayment and save a good chunk of money.

But refinancing your student loan doesn’t have to be a one-and-done strategy. Refinancing student loans multiple times is possible and, in fact, we recommend it.

Regularly refinancing student loans can make financial sense

Through the refinancing ladder strategy, you start out with a longer term and refinance several times more with shorter repayment terms. This strategy works if you use that saved money in interest and throw more toward your principal balance.

Student loan refinancing is the only meaningful way to significantly reduce your interest rate (autopay discounts can account for a 0.25% reduction). Let’s take a look at some examples:

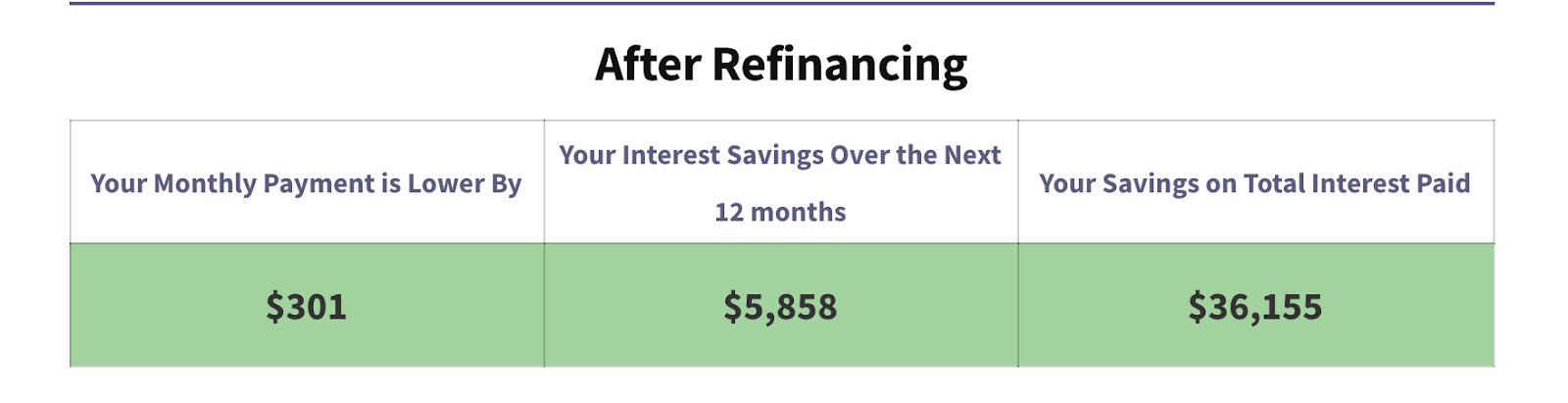

Let’s assume you have $300,000 in student loan debt with a 7% interest rate with 10 years to pay off your loan. You get approved to refinance, and you’re offered a 5% interest rate thanks to your strong credit score of 700, and you choose a 10-year repayment term.

By refinancing alone, your monthly payment is reduced by $300. Imagine what you could do with that amount of money each month. Paying down your debt faster is just one option. Over the life of your loan, you’ll save more than $36,000.

In our latest refinancing survey, we found that 80% of respondents would need an interest rate reduction of at least 1% to make refinancing worth it.

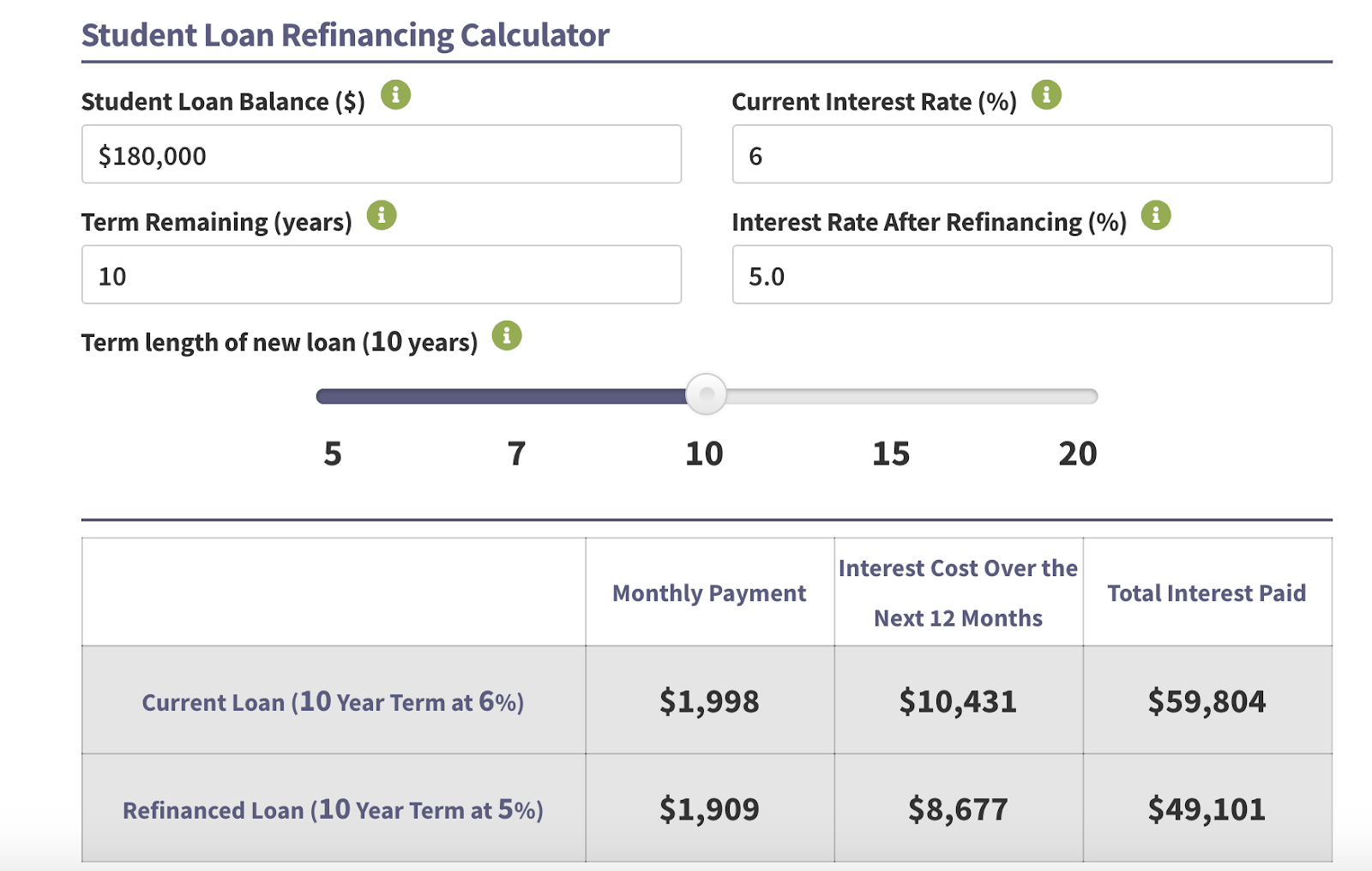

Let’s say you owe $180,000 with an interest rate of 6% and had 10 years to pay it off. During a refinance, you choose a repayment term of 10 years at 5% interest. Not only will your monthly payment decrease, but you’ll save nearly $10,000 overall.

We surveyed over 3,200 respondents and many of them owe more than six figures of student loan debt (56%), while 40% of respondents had a six-figure income.

What’s interesting is that many respondents said they’d be okay with refinancing student loans multiple times because of cash bonuses. At Student Loan Planner®, we offer lucrative cash back bonuses of up to $1,000 or more across all of our refinancing partners.

Eighty percent of respondents with private loans said they’d refinance again for a $1,000 cash bonus, but a similar percentage would only refinance if they scored at least a 1% interest rate reduction.

But here’s the thing. A reduction of just 0.5% could save you even more than the bonus, illustrating that many people are lured in by short-term bonuses rather than long-term gains.

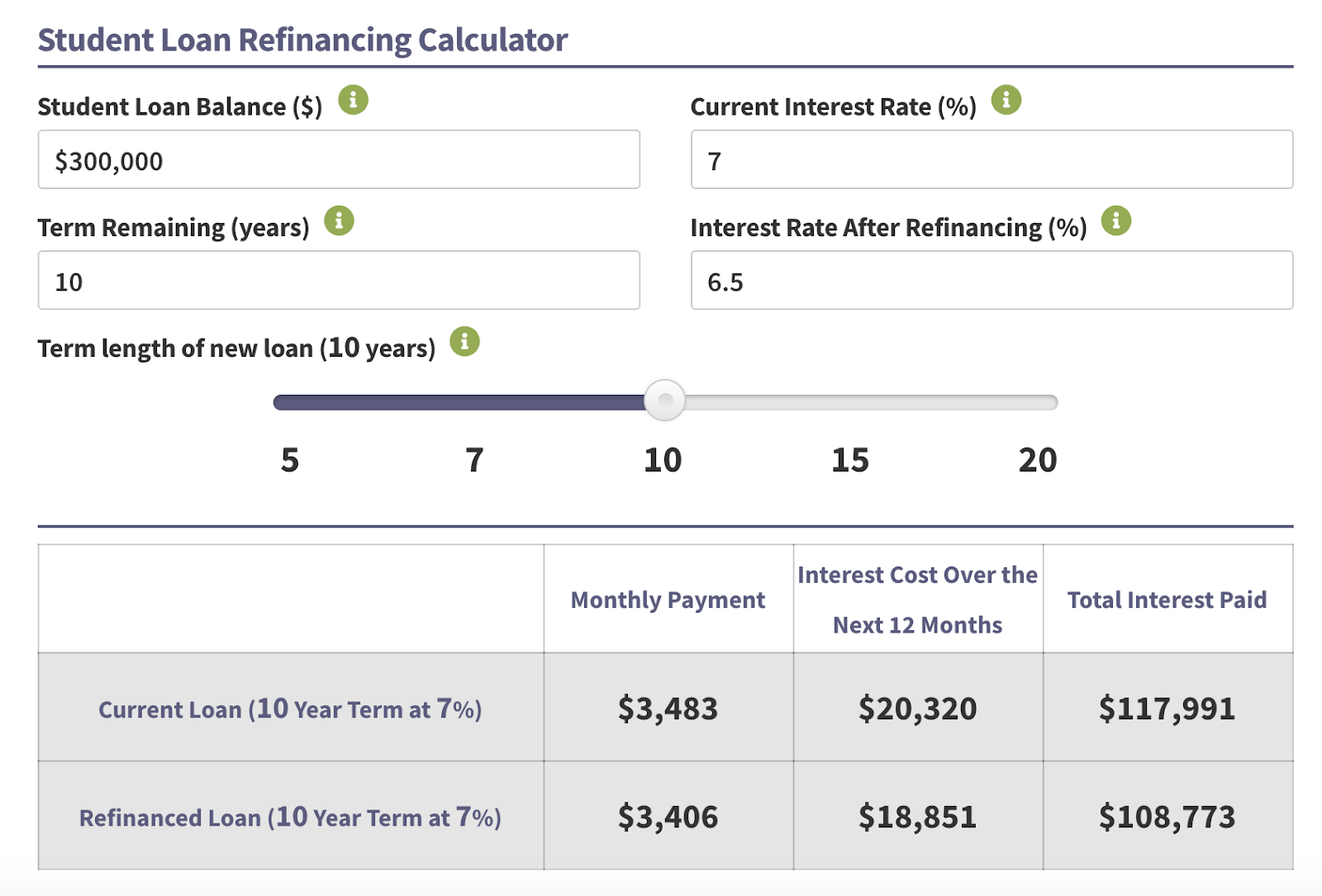

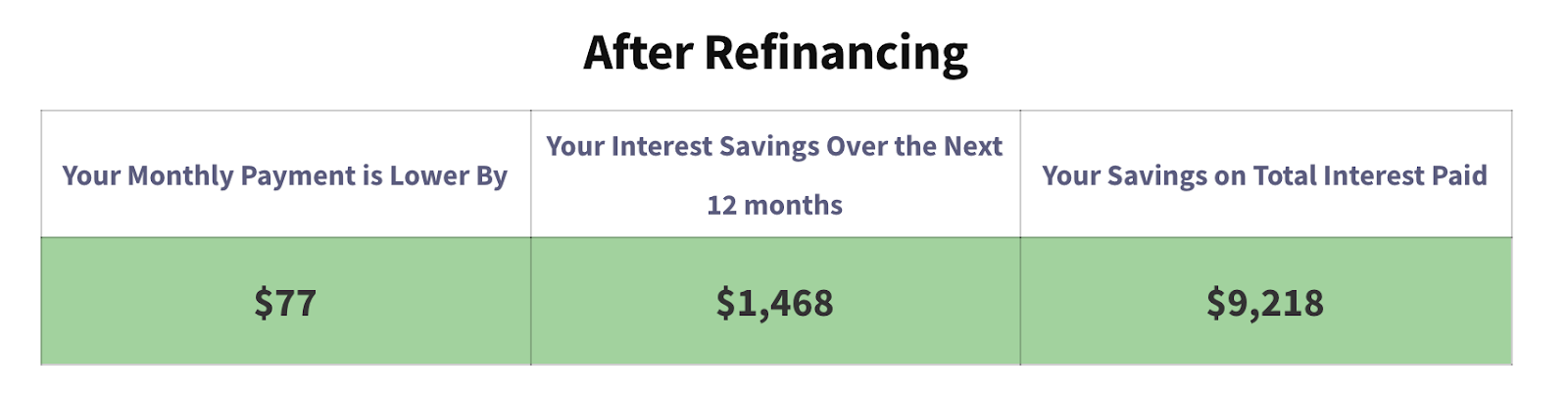

Let’s go back to our example of a high-debt student loan borrower with $300,000 of debt at a 7% rate. Refinancing at a 6.5% rate with a 10-year repayment term results in more than $1,000 savings in the first year alone. Over the life of the loan, that’s nearly $10,000!

Want to check out your own student loan refinance savings calculations? Check out our student loan refinancing calculator yourself.

What to know before refinancing student loans multiple times

Although refinancing student loans multiple times is possible, it’s best to avoid refinancing too frequently. You don’t want to refinance your student loans every month, for example.

But a good refinancing benchmark is every two years or so, with a minimum of one year. Much of this has to do with your credit. When you take out a new loan, your credit score takes a small hit as there’s a ‘hard inquiry’ on your credit report.

According to the credit bureau, Experian, a hard inquiry will fall off your report in two years and will no longer affect your credit after one year.

You want to keep tabs on your credit and make sure it’s the same or improved by the time you refinance again. You can review your credit report for free at AnnualCreditReport.com and check your credit score with your financial institution, credit card or a third-party credit score platform like Credit Karma.

It’s important to understand how your repayment term affects your total monthly payment and how much interest you’ll pay over time. The longer the repayment term, the smaller the payment amount due, but you’ll pay the price in interest long term.

The shorter the repayment term, the higher your monthly payment is, but you’ll pay less in interest. Also, check out each refinancing lender’s specific perks. For example, SoFi® offers features like financial planning from credentialed advisors.

Is it bad to refinance student loans multiple times?

Refinancing student loans multiple times isn’t bad in and of itself. Of course, whether it’s a good idea depends on your personal situation. If your credit is shot or you’re dealing with unemployment or underemployment, now might not be the time to refinance again.

Also, our survey found that many people are holding off on paying back their loans until the federal payment freeze expires. A total of 25% of respondents are waiting to see if President Biden will cancel student loans or offer student loan forgiveness.

Another 18% of borrowers are holding off because of income-driven repayment forgiveness and another 18% is holding off because of Public Service Loan Forgiveness (PSLF). Currently, the federal deferment on student loan payments still counts toward loan forgiveness, so this approach makes sense.

If you’re considering refinancing for the first time and have federal student loans, it’s wise to wait until the student loan payment pause is over to reassess your student loan situation. Student loan refinancing isn’t a good idea if you want to pursue loan forgiveness or opt for income-driven repayment.

Guide to refinancing student loans multiple times

If you’ve already refinanced student loans, you likely know a bit about the process. But here’s a good checklist of what to do when refinancing student loans multiple times.

- Check your debt-to-income ratio (DTI). Each lender has its own income requirements. An important number to know is your debt-to-income ratio which should be less than 50%. To calculate your DTI, add your total monthly payments and divide it by your monthly income. For example, if your income is $5,000 per month and your total debt payments equal $2,000, your DTI is 40%.

- Review your credit score. Again, each refinancing lender has different credit requirements but a good benchmark is 650 or above.

- Look at rates and cash back bonuses. To get the best deal, review multiple student loan refinancing lenders to compare rates and cash-back bonuses.

- Gather your personal and loan info. Have your pay stubs, tax returns, address, and Social Security number handy when applying for another refinancing loan. Review how much student loan debt you have, so you know how much you need to borrow for a refinance.

- Get quotes from several lenders. Our survey found that a third of respondents applied with one refinancing lender. Make sure you request quotes from multiple refinancing lenders to ensure you’re getting the best rates and terms.

SoFi®, Laurel Road and Earnest make up roughly 50% of the refinancing market. If you’re looking for a starting point, these are good options to check out.

Bottom line

Now, you can stop wondering how often you can refinance student loans. There’s no restriction.

Refinancing student loans multiple times can be a smart financial strategy when done right, especially with the refinancing ladder approach we mentioned above. But of course, it all depends on your personal financial situation.

Do you have any questions or concerns about refinancing (again)? Get in touch for a student debt consult.

Refinance student loans, get a bonus in 2025

| Lender Name | Lender | Offer | Learn more |

|---|---|---|---|

|

$500 Bonus

Bonus for eligible users who refinance $100k or more (bonus from SLP, not SoFi)

|

Fixed 4.49 - 9.99% APR

Variable 5.99 - 9.99% APR with all discounts with all discounts |

|

|

$1,000 Bonus

For 100k or more. $200 for 50k to $99,999

|

Fixed 4.79 - 9.99% APR

Variable 5.88 - 9.99% APR

|

|

|

$1,000 Bonus

For 100k or more. $300 for 50k to $99,999

|

Fixed 4.25 - 10.24% APPR

Variable 4.86 - 10.24% APR

|

|

|

$1,050 Bonus

For 100k+, $300 for 50k to 99k.

|

Fixed 4.74 - 8.75% APR

Variable 5.04 - 9.05% APR

|

|

|

$1,099 Bonus

For 150k+, $300 to $500 for 50k to 149k.

|

Fixed 4.88 - 8.44% APR

Variable 4.74 - 8.24% APR

|

|

|

$1,250 Bonus

For 100k+, $350 for 50k to 100k. $100 for 5k to 50k

|

Fixed 3.99 - 10.30% APR

Variable 4.20 - 11.41% APR with autopay with autopay |

Not sure what to do with your student loans?

Take our 11-question quiz to get a personalized recommendation for 2025 on whether you should pursue PSLF, SAVE or another IDR plan, or refinancing (including the one lender we think could give you the best rate).