Until July 2025, Parent PLUS borrowers can obtain the best income-driven repayment (IDR) plans out there, including the Saving on a Valuable Education (SAVE) plan, if they consolidate their loans twice. This is called the double consolidation loophole.

But once that loophole closes, far fewer borrowers with Parent PLUS loans will be able to get forgiveness.

Who among Parent PLUS borrowers should pursue forgiveness after this loophole closes in 2025? We’ll show you how to navigate your post-double-consolidation options.

Why the ICR plan will determine who can get forgiveness on Parent PLUS

After the double consolidation loophole closes, only new Parent PLUS loan borrowers who enroll in Income-Contingent Repayment (ICR) can get forgiveness (this doesn’t apply to folks who finish the double consolidation loophole by July 2025).

What is the ICR plan you ask?

It’s a complex formula that uses 100% of the poverty line as a deduction (compare this to 150% of the poverty line with Income-Based Repayment or 225% of the poverty line with SAVE).

So, for ICR, you take your adjusted gross income (AGI) minus 100% of the poverty line and multiply by 20% to get your payment.

Is there a cap on ICR?

Yes, it’s the standard 12-year amortization multiplied by an income-sensitive factor ranging from about 0.5 to 2.

- For lower-income borrowers, the cap is something like a 24-year standard plan amortization.

- For higher-income borrowers, the cap is closer to a 6-year standard plan.

Confused yet? I don’t blame you. The ICR formula and cap are relevant because you need to get a low enough payment to qualify for forgiveness under ICR after 2025, or you won’t be able to pursue forgiveness on Parent PLUS loans.

Let’s talk about the five key strategies Parent PLUS borrowers need to get forgiveness if they don’t make the double consolidation deadline.

1. Keep Parent PLUS loans in the name of the lower-income spouse

Once the double consolidation goes away, you won’t be able to get a low payment unless you borrow all of the Parent PLUS loans in the name of the lower-income spouse (if married).

If one spouse is a teacher, social worker, or stay-at-home parent and the other is a lawyer, physician or engineer, you’ll want the first spouse to borrow ALL of the Parent PLUS debt.

This will enable you to keep monthly payments very low.

2. Defer payments for the Parent PLUS borrower for as long as possible

If you borrow Parent PLUS, you can defer payments as long as you have one child in school. Then, you can forbear for up to three years after everyone has graduated by requesting an economic hardship forbearance.

This strategy can put off payments that would be very high as a percent of your income.

3. Generate low income for the Parent PLUS borrower in retirement

The best way to get forgiveness on Parent PLUS after the double consolidation will be to have the Parent PLUS borrower keep their AGI quite low.

That means a borrower who would be a good forgiveness candidate would have modest retirement income, such as primarily Social Security and required minimum distributions (RMDs) from 401k plans or IRAs.

Many folks generate only $10,000 to $40,000 of taxable income in retirement. Such a person would be an excellent forgiveness candidate. But ignoring your withdrawal strategy could jeopardize your chances of getting forgiveness.

4. Your spouse needs to earn less than six figures

If your spouse earns $100,000 or more and will continue to earn that amount long into retirement, the cost of filing taxes separately could be pretty high, particularly if your spouse is signing up for Medicare.

You need to file separately for Parent PLUS forgiveness to avoid having to include your spouse’s income in your monthly payment calculation.

If you earn $30,000 and your spouse earns $70,000, the cost of filing separately is about $1,700 a year.

If you earn $30,000 and your spouse earns $120,000, the cost of filing separately would be about $9,100 (primarily from higher Medicare premiums for the high-earning spouse).

So, realistically, if your spouse has six-figure earnings, you’ll struggle to get forgiveness after the double consolidation loophole ends.

5. Parent PLUS borrowers with six-figure debts have the easiest forgiveness path

If you owe a common $20,000 to $50,000 Parent PLUS balance, you’ll have a hard time justifying pursuing forgiveness. Why? Because Parent PLUS forgiveness comes with a lot of complexity and added tax costs.

However, borrowers with over $100,000 of debt could be excellent forgiveness cases because pursuing full repayment would require major life sacrifices.

Many borrowers with six-figure Parent PLUS balances would have to put off retirement for years if they paid off all their debt.

Who could change their life with Parent PLUS forgiveness through ICR?

Here are the types of borrowers who should consider pursuing Parent PLUS forgiveness even after the double consolidation loophole ends:

- When retired, you and your spouse will each earn less than a six-figure income.

- You have six figures of Parent PLUS debt, taken out by the spouse with the lower income.

- You have multiple children you’re borrowing for, especially if they attend expensive schools.

- You’re able to keep your taxable retirement income moderate because you can tap into income from other non-taxable sources, such as Roth IRAs.

Example of ICR Parent PLUS forgiveness

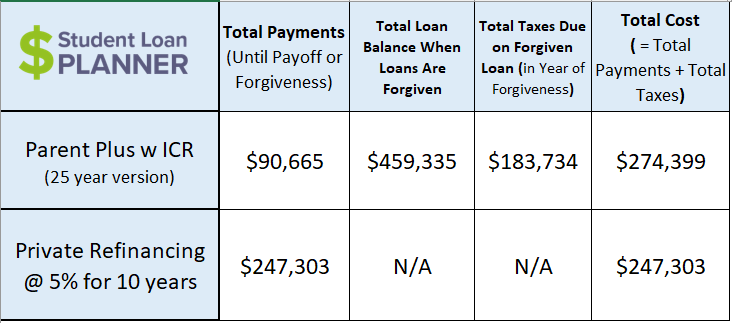

Assume you earn $30,000 a year, and your spouse earns $70,000 a year. You have $200,000 of Parent PLUS debt. Here’s your total costs if you file taxes separately:

You’ll notice that if you must pay taxes on the forgiven amount at the end, the cost is still quite high. However, due to political realities, that’s very unlikely.

If you add about $2,000 a year of tax costs from filing separately for 25 years, the total cost is $90,000 + $50,000 = $140,000.

When spread out over 25 years, it still looks quite moderate compared to paying nearly $250,000 of principal and interest over 10 years.

However, if this same borrower finished the double consolidation before July 2025, they’d pay $0 a month under the SAVE plan, and their interest would be subsidized, so the balance wouldn’t grow.

Even if a court reverses the SAVE plan one day, whatever plan that replaces it would likely still offer extremely low payments.

Get help with Parent PLUS debt before loopholes end

If you want to benefit from the double consolidation before it’s over, get a consult with our team of experts.

While ICR Parent PLUS Forgiveness is still a valid path for some after the loophole ends, it’s nowhere near as cheap as double consolidation if your final child will not need to borrow in 2025.

Refinance student loans, get a bonus in 2025

| Lender Name | Lender | Offer | Learn more |

|---|---|---|---|

|

$500 Bonus

For refinancing 100k or more (bonus from Student Loan Planner®, not SoFi®)

|

Fixed 4.49 - 9.99% APR

Variable 5.99 - 9.99% APR with all discounts with all discounts |

|

|

$1,000 Bonus

For 100k or more. $200 for 50k to $99,999

|

Fixed 4.45 - 9.89% APR

Variable 5.88 - 9.99% APR

|

|

|

$1,000 Bonus

For 100k or more. $300 for 50k to $99,999

|

Fixed 4.29 - 10.24% APPR

Variable 4.86 - 10.24% APR

|

|

|

$1,050 Bonus

For 100k+, $300 for 50k to 99k.

|

Fixed 4.99 - 8.90% APR

Variable 5.29 - 9.20% APR

|

|

|

$1,099 Bonus

For 150k+, $300 to $500 for 50k to 149k.

|

Fixed 4.88 - 8.44% APR

Variable 4.86 - 8.24% APR

|

|

|

$1,250 Bonus

For 100k+, $350 for 50k to 100k. $100 for 5k to 50k

|

Fixed 3.85 - 11.69% APR

Variable 4.35 - 12.68% APR with autopay with autopay |

Not sure what to do with your student loans?

Take our 11-question quiz to get a personalized recommendation for 2025 on whether you should pursue PSLF, SAVE or another IDR plan, or refinancing (including the one lender we think could give you the best rate).