The federal student loan payment and interest pause is set to expire in August, with payments restarted on September 1, 2023. Borrowers must prepare to resume payments after an almost two-year freeze. Those who are on an income-driven repayment (IDR) plan will need to recertify student loans in the near future to account for changes in income and family size.

Here’s how to recertify your income-driven repayment plan after the COVID-19 administrative forbearance ends.

What to expect when federal student loan repayment resumes

According to the Department of Education, following the end of the payment suspension period, federal student loan borrowers will need to make payments starting October 1, 2023.

When your payment resumes, you should expect to pay the same amount as what you were paying before the administrative forbearance took effect. That monthly payment amount will continue until your IDR recertification date comes into play.

Student loan recertification after the payment pause ends

Borrowers making payments under an IDR plan must recertify their income and family size each year. But the COVID-19 administrative forbearance period has made this process a little more complicated, considering borrowers have had $0 payments for almost two years without the need to recertify student loans.

So, what does this mean for borrowers in terms of submitting their annual student loan recertification application?

StudentAid.gov details that you don’t have to recertify your income before the end of the payment freeze. This is the case even if your original recertification date has come and gone during this emergency relief period.

Your loan servicer will notify you of your new annual deadline to recertify student loans. Recertification dates will vary by borrower, so check with your loan servicer directly.

For reference, my student loans serviced by Navient — which recently announced its exit as a federal student loan servicer — are showing that my IDR plan is set to expire in January 2024. That’s a significant amount of time to readjust to making payments before recertifying.

Depending on your new recertification date, you might want to re-certify early if your income has dropped during the pandemic, if your family size has grown or if you want to change to another IDR plan that’s more beneficial.

How to recertify your income-driven repayment plan

When you’re ready to recertify your student loans (whether it’s early or in accordance with your new recertification deadline), start with FSA ID and password to log into your StudentAid.gov account to apply for recertification.

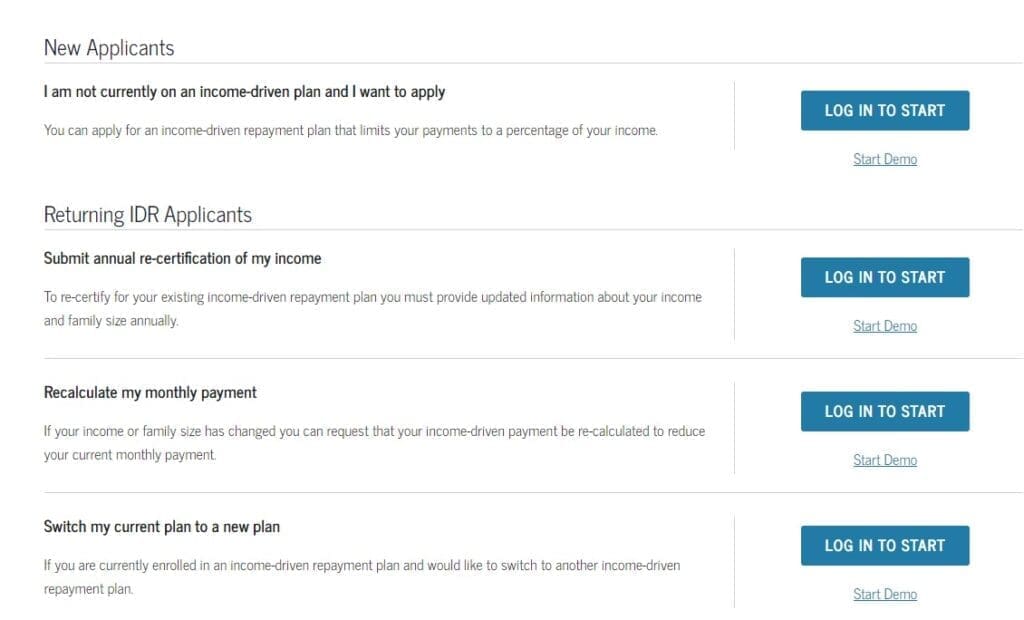

Look for the area that splits up application actions between “New Applicants” and “Returning IDR Applicants”.

Depending on your situation, select the appropriate button.

To simply recertify your income under your existing IDR plan, click “Submit Re-Certification” to begin the student loan recertification process.

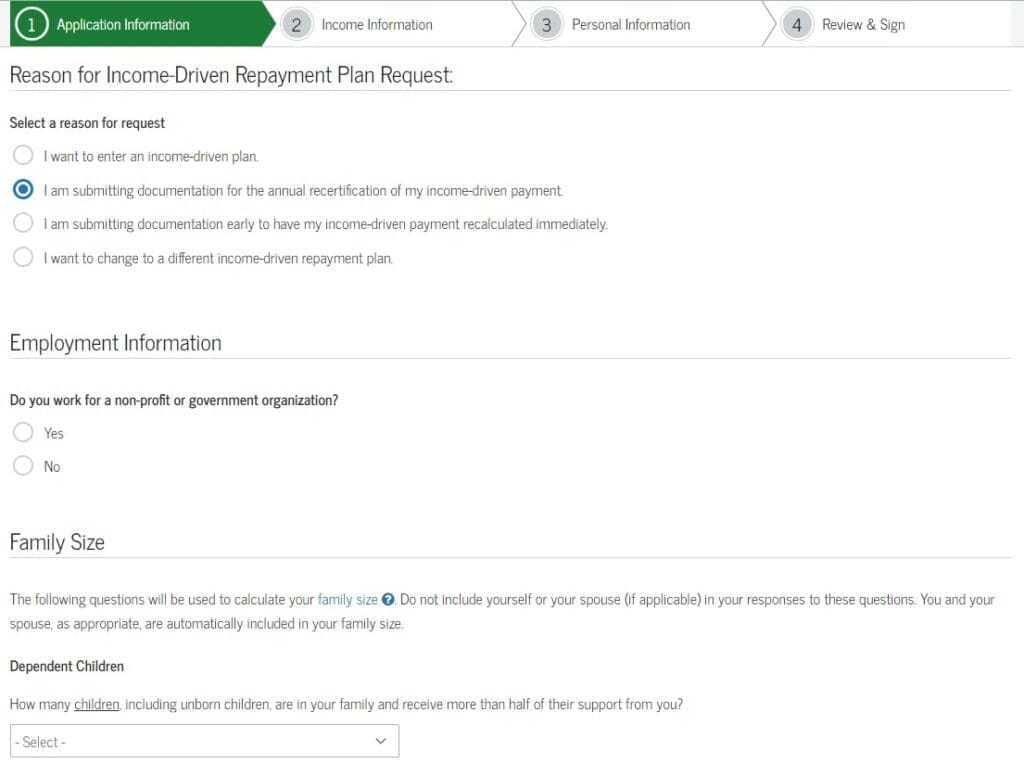

Step 1: Submit application information

Start by entering your general application information, ensuring that you’ve selected the correct reason for your IDR plan request.

In this case, it would be “I am submitting documentation for the annual recertification of my income-driven payment.”

You’ll also select details related to your employment information, family size and marital status.

Keep in mind you can include unborn children in your dependent count if you or your spouse is currently pregnant.

Step 2: Verify income information

Next, you’ll provide income information using the IRS Data Retrieval Tool to transfer your recent tax return information into your recertification application. This tool eliminates the need for additional income documentation.

Related: To Link or Not to Link: Guide to IRS Automatic Income Sharing for Student Loans Repayments

However, if your income is significantly different from your most recent tax return, you can submit further income documentation manually to your loan servicer.

Your loan servicer will provide instructions along with acceptable income documentation formats. Supporting income documentation might include:

- A pay stub or letter from your employer detailing your gross pay

- Appropriate documentation for each source of income

- A signed statement explaining your income sources

For married borrowers, you’ll also need to indicate whether you file taxes separately or jointly. Be prepared to provide information related to your spouse’s income information.

Note that in very specific circumstances, you can indicate that you aren’t able to access your spouse’s income (e.g. victims of domestic violence or going through a separation). But don’t choose this option lightly if it isn't truthful as it’ll be considered fraud.

Step 3: Confirm your personal information

Once all income information has been transferred, you’ll submit personal information related to your permanent address and contact information.

This is a straightforward step, but always double-check that your contact information is correct.

Step 4: Review your application and sign

Review all of your application information for accuracy before signing it. If you see any mistakes, select the edit button and make the necessary changes.

It’s important that all provided information is correct and true. Don’t falsify or misrepresent information as this can result in penalties, such as fines or imprisonment (or both).

If your recertification application is complete, read through the final details to understand the terms you’re agreeing to. Then, certify and sign the application.

Your loan servicer will contact you if any additional information or documentation is needed. Continue making your normal payments until you’re notified otherwise.

Be strategic about your IDR plan payment

As a reminder, your monthly payment is calculated based on a percentage (ranging from 10% to 20%) of your discretionary income. This is generally determined by your adjusted gross income (AGI) and family size.

IDR plans include:

- Saving on a Valuable Education (SAVE)

- Pay As You Earn (PAYE)

- Income-Based Repayment (IBR)

- Income-Contingent Repayment (ICR)

Your loan servicer will calculate your income using your most recent federal income tax return. But if you haven’t filed yet, you can use an older tax return which might reflect a lower AGI than your present income. This can help keep your payments lower for another year.

The important thing is being truthful about your tax information and income, while also being strategic about your student loan payments.

If your income increased during the pandemic, wait until your recertification deadline to provide updated income information since you’re not required to give it to your servicer sooner.

However, if your income dropped, submit documentation to recalculate your monthly IDR payment. Take advantage of the lower monthly payment anytime you can.

Need help with determining the best student loan repayment strategy? Book a one-hour consultation with our student debt experts.

Not sure what to do with your student loans?

Take our 11 question quiz to get a personalized recommendation for 2025 on whether you should pursue PSLF, IDR, or refinancing (including the one lender we think could give you the best rate).