The Double Debt Loophole is a strategy to squeeze every last bit of efficiency out of a couple’s income-driven repayment (IDR) towards forgiveness. If you’re going the forgiveness route, you want to minimize your payment as much as possible to maximize how much you get forgiven.

Let’s talk about what you can do to maximize the Double Debt Loophole.

Who should consider this strategy

Filing taxes separately to exclude spousal income from their payment is a common strategy for married borrowers where only one spouse has the student debt. It’s also necessary to carry out the Double Debt Loophole when both spouses have student debt.

You should consider this strategy when student loan forgiveness is inevitable (PSLF or private sector), and you meet one of the following scenarios.

Scenario 1: Both spouses earn similar annual incomes with a big discrepancy between student loan amounts

If you have student loans and make about the same as your spouse, you might benefit from the Double Debt Loophole if the balances of your student loans are very different.

For borrowers living in a community property state (Arizona, California, Idaho, Louisiana, New Mexico, Nevada, Texas, Washington and Wisconsin), you could still benefit even if your spouse makes significantly more or less than you. This is because income is divided between both spouses equally on their federal income tax return/1040 if filing taxes separately using the 8958 form.

This essentially makes you and your spouse’s AGI appear to be the same. Thus, making you a good candidate for the Double Debt Loophole via the Community Property State Loophole. A loophole within a loophole!

Scenario 2: Both spouses owe about the same in federal student loan debt, but there's a big discrepancy in spousal income

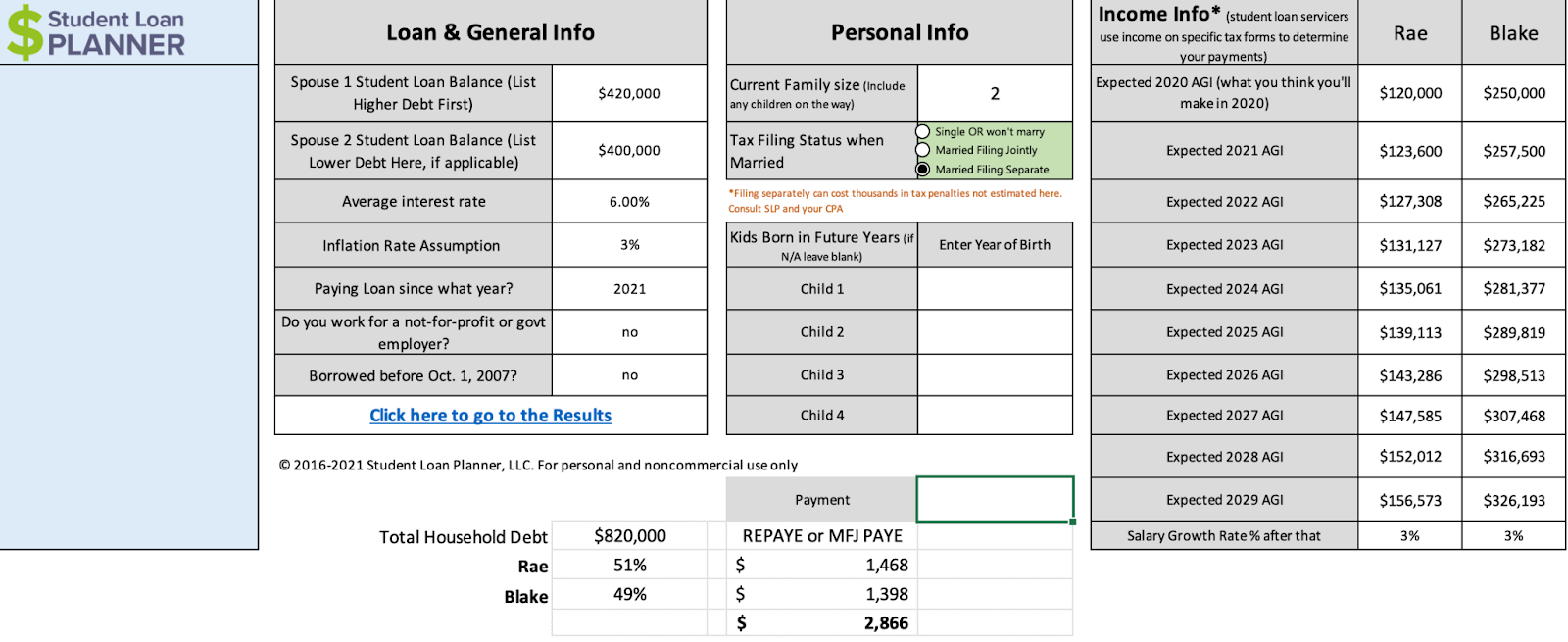

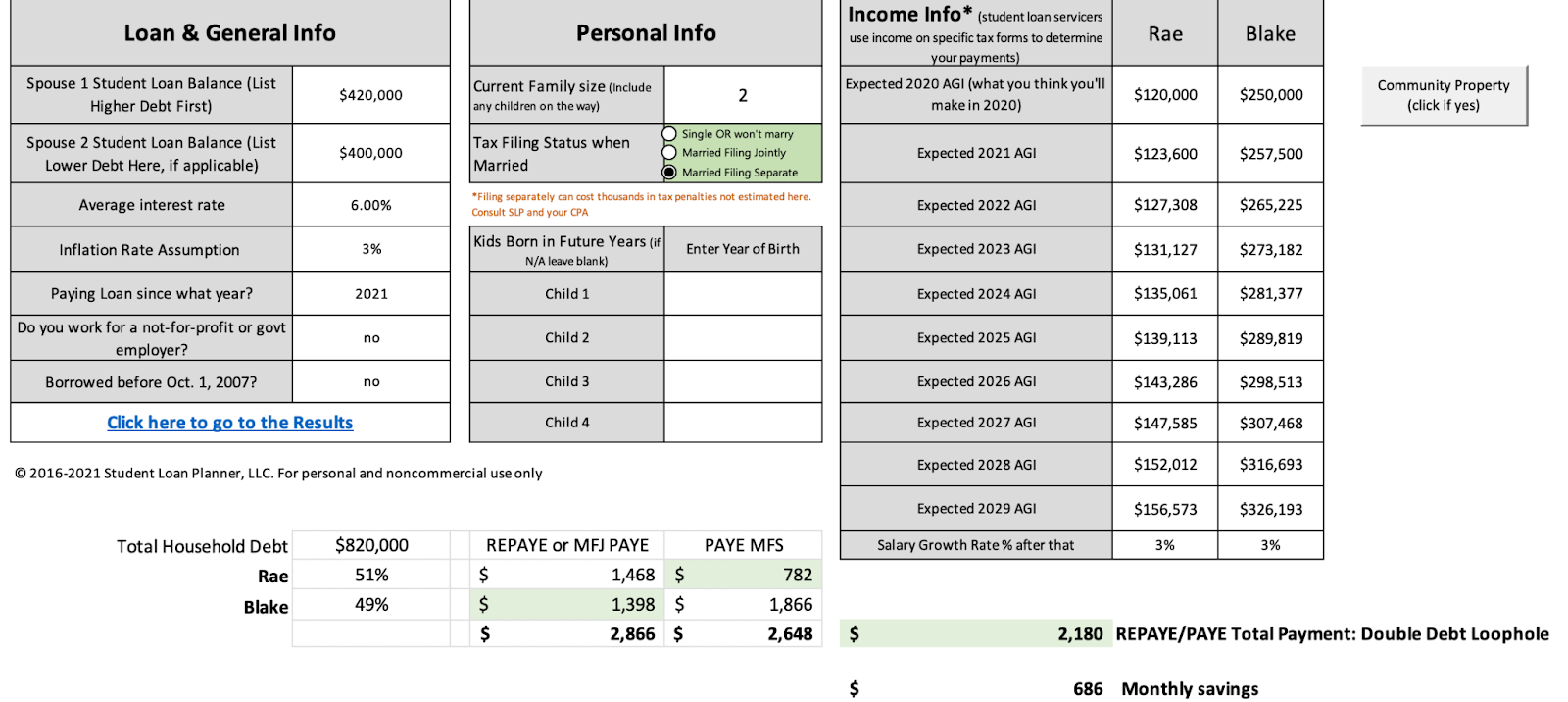

Let’s take another example and say Rae and Blake both owe about the same in student loans. Rae owes $420,000, and Blake owes $400,000.

Their individual income is quite different, though: Rae earns $120,000 per year, and Blake earns $250,000 per year. Rae’s going for taxable forgiveness on the Pay As You Earn (PAYE) plan after 20 years. Blake’s planning for Public Service Loan Forgiveness (PSLF). Both are eligible for the Revised Pay As You Earn (REPAYE) and PAYE payment plans.

If they filed taxes jointly or both went on REPAYE (this plan always considers joint income when calculating the payment amount), their combined income would be considered. However, their individual payment responsibility will be based on their proportionate debt load.

What does this mean? Let’s do the math for their payment, assuming they’re both on REPAYE or filing taxes jointly on the PAYE plan:

With a two-person family size, the total household payment for an AGI of $370,000 would be $2866 per month.

- Rae’s Payment Proportion: $2,866 x 51% = $1,468 per month

- Blake’s Payment Proportion: $2,866 x 49% = $1,398 per month

Rae makes 48% less income than Blake. Yet, her monthly payment is slightly more than Blake’s because of how the federal system divides the payment between student loan borrowers filing taxes jointly. This is also the case when both borrowers are on REPAYE.

This is tough for Rae because she’s personally no longer benefiting from the IDR plan like she would if her payment was truly just based on just her own discretionary income. In other words: She’s not achieving the goal of reducing her payment as much as possible to maximize her forgiveness.

The difference between filing taxes separately

Filing taxes separately allows you to base your payment on your own income on the PAYE and Income-Based Repayment (IBR) plans. Whereas REPAYE always considers your spouse’s income regardless of tax filing status. These facts are important to remember.

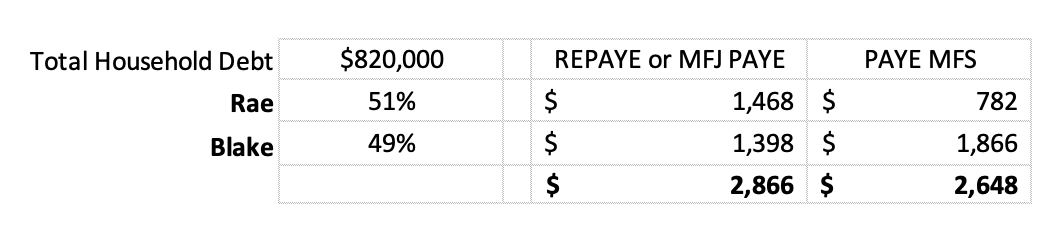

Let’s run the numbers for Rae and Blake if they choose married filing separately (MFS) and apply for PAYE to compare to the above scenario:

Rae’s repayment amount drops quite a bit, saving her $686 per month! But Blake’s payment goes up because his income is higher, and he’s no longer participating in the lower payment proportion if he were to go on PAYE. This is because PAYE uses his own income to calculate the payment when filing taxes separately.

Insert Double Debt Loophole here: Let’s assume Blake goes on REPAYE and Rae goes on PAYE. Why? Think back: Blake benefits from having his payment proportionalized because his balance is slightly lower than Rae’s.

Rae doesn’t benefit from REPAYE but would benefit from PAYE, allowing her to calculate her payments based on her own income if they file taxes separately:

So, if Blake applied for REPAYE, and Rae applied for PAYE, and they filed taxes separately, their total payment would be $2,180 per month, versus $2,648 if both were on PAYE filing taxes separately or $2,866 if both were on REPAYE/filing taxes joint.

How to implement this strategy

Step 1: Consider filing taxes separately next time

Your upcoming 2022 taxes may be the next opportunity to consider filing taxes separately with your spouse.

We’re still in the midst of the CARES Act student loan payment relief, which froze federal student loan payments until August 30, 2023.

When President Biden's Department of Education lifts the payment freeze, your IDR payment will resume at what it was prior to your payments being suspended unless you intentionally recalculated your payment since March 2020.

If you’re new to repayment and want to enroll for an IDR plan now, the application links back to your most recently filed IRS tax return, pulling through your AGI (Adjusted Gross Income) to calculate your payment.

This means that if your most recent tax return on file isn’t already filed separately, you might not be able to implement this Double Debt Loophole strategy immediately. But you could re-calculate your payments after 2022 taxes are filed separately.

The hidden costs of filing taxes separately

Keep in mind there can be downsides to filing taxes separately that you should evaluate as well. Make sure that the potential consequences of filing separately don’t erode this strategy’s cost savings.

Schedule a free 15-minute consultation with Student Loan Tax Experts or another qualified tax professional to discuss the tax implications for filing taxes separately.

Here are some of the tax benefits you could be giving up when you file taxes separately because they’re for married couples filing jointly:

- Education credits or student loan interest deduction of $2,500.

- Potentially more advantageous tax brackets.

- Child care tax credit.

- Earned income tax credit.

- Exclusion or credit for adoption expenses.

- Ability to contribute to a Roth IRA (however, you can overcome this by doing a Backdoor Roth IRA conversion).

- Ability to deduct rental property losses.

- Ability to take the standard deduction if one spouse itemizes.

Step 2: Apply for the respective income-driven repayment plan

Submit your application for an income-driven repayment plan. Make sure that the correct tax return pulls through on the application. If not, close out of it and wait a few weeks before applying. Sometimes a tax return can take a few weeks to reflect for the IRS data retrieval tool within the income-driven application.

Related: To Link or Not to Link: Guide to IRS Automatic Income Sharing for Student Loans Repayments

Who goes on REPAYE?

The spouse with the lowest student loan balance goes on REPAYE to reap the benefit of the proportionate payment allocation.

Who goes on PAYE or IBR?

The spouse with the lower income or the higher balance goes on PAYE or IBR.

Make sure to sign off on each other's applications. The Department of Ed makes spouses “co-sign” an income-driven application to:

- Confirm you’re married (you get a larger poverty-line deduction for being married).

- Confirm you both filed taxes the same way.

- “Link” you two together for the payment calculation.

Signing off on each other's applications does NOT obligate you to your spouse’s loans in any way. I know, I know… I wish they’d change the terminology from cosign to something else!

Step 3: Make your payments

Also, confirm you are on track for Public Service Loan Forgiveness if applicable. This includes submitting an Employment Certification Form (ECF) at least once annually.

Hire help to take advantage of the Double Debt loophole

I know this loophole can make your head spin. Not sure if this strategy could work for you and your spouse? Do you have the added complexity of living in a community property state? Schedule a consultation with us for your customized student loan plan.

Not sure what to do with your student loans?

Take our 11 question quiz to get a personalized recommendation for 2025 on whether you should pursue PSLF, IDR, or refinancing (including the one lender we think could give you the best rate).

Comments are closed.