Editor's note: Fraud is a legal definition, and the following article serves to provide our opinion that answering that you're married but cannot reasonably access your spouse's income information on IDR recertification is usually fraud, unless there is a specific reason such as spousal abandonment, separation, or abuse which makes that answer accurate. The question is most commonly utilized to incorrectly exclude spousal income from the Revised Pay As You Earn (REPAYE) repayment program.

As a student loan consultant, I'm frequently asked something like: “I have this great low monthly payment, but I’m a little nervous. On my income-driven repayment certification each year, I check a box that says that I’m married but cannot reasonably access my spouse’s income information.’ Is this something I could get in trouble for?”

The short answer is yes. In most cases, this is fraud or, at minimum, intentionally inaccurate.

We’ll cover why that is, and why you don’t even need to check this box to reduce your student loan payments in most cases for income-driven repayment.

Why does the government want to access your spouse’s income information as a student loan borrower?

The majority of student loan borrowers now sign up to pay their federal student loans on an income-driven repayment (IDR) plan. These student loan repayment options lower payments compared to a Standard Repayment plan and can help your financial situation.

Long term, a majority of Americans still get married at some point in their lives. This is particularly true for those with higher education levels.

When calculating your payment amount for federal income-driven repayment programs, the government includes your spouse’s income — so your combined income — if your tax filing status is “married filing jointly.”

If you and your spouse both have Direct loans, then you can split that payment proportionally. Your payments will be based on what percentage of the total amount each of you owes.

However, if you’re the only one with student debt, getting married can cause your payment to go up. This is the case even if your spouse had nothing to do with borrowing that money.

Some people believe this is unfair. That feeling might cause married borrowers to rationalize seeking to avoid giving the government information on their spouse’s income/joint income throughout their repayment period.

Why borrowers check ‘can’t access my spouse’s income’

Imagine you have an outstanding loan balance of $200,000 in student loan debt. You earn $50,000 a year and have a spouse who earns $50,000 a year also.

If you filed a joint federal income tax return, you would have to pay $618 a month. If you checked “can’t access my spouse’s income,” you might be able to pay as little as $201 a month.

That’s almost a $5,000 per year incentive to fudge the numbers.

What is the ‘can’t access spouse’s income’ box intended for?

If you look at the history and commentary around adding the “married, but cannot reasonably access my spouse’s income information” box to the income-driven repayment plan request form, it’s intended to be for:

- Victims of domestic violence

- Spouses in the process of separating

- Spouses living apart

- Situations in which one spouse might be in another country, such as being on a military deployment

If you live in the same household, you can reasonably access your spouse’s income unless you fall into one of the categories listed above.

I’ve heard borrowers try to justify their response. For example, I've heard, “Well you don’t understand. My husband literally will refuse to give me his income because it's ‘none of my business.’”

There is a much better way to achieve the goal of paying less on your student loans by signing up for the most advantageous IDR plan. Choose the Income-Based Repayment Plan (IBR) or Pay As You Earn (PAYE) repayment plan and file separate federal income tax returns.

Additionally, Biden and the Department of Education unveiled a new payment plan called SAVE, which replaces REPAYE as we know it. According to StudentAid.gov, a major change from REPAYE to SAVE is that your spouse's income can be excluded if you're married and file taxes with the IRS separately.

This loan repayment plan also increases the poverty guideline, which is used with your adjusted gross income (AGI) to calculate payments based on discretionary income. Another major perk is that unpaid interest on subsidized and unsubsidized loans is eliminated when you make a payment. So your total balance won't balloon out of control.

While the income-contingent repayment plan (ICR) is part of IDR, it's generally not recommended if other options are available.

How to avoid paying on your spouse’s income under IBR plans

The American student loan system is complicated, but it gives you the ability to exclude your spouse’s income completely legally.

Perhaps it should be easier. I’m not the one who designed the system. I just want to help you successfully navigate it.

Let's say the borrower mentioned above with the $50,000 income filed separately from her spouse earning $50,000 for taxes. Then, she could legally exclude her spouse’s income from calculating her PAYE plan payment. That $201 payment per month would be the result.

You can’t trust your loan servicer

I’ve heard many borrowers justify their response to the “can’t access spouse’s income” box because they claimed their servicer told them to say that. I totally believe them!

Call center customer service quality at the loan servicers is atrocious. The phone reps generally have a script that says to recommend the REPAYE program (now SAVE) in basically every situation, even if an alternative repayment plan might be better for you.

So, a phone rep who doesn’t care or who’s in a rush is likely to tell borrowers to do something that’s not correct to speed up the conversation.

Other rulings with programs such as Public Service Loan Forgiveness (PSLF) have found that loan servicing reps cannot promise anything to you. Many borrowers were told they were building qualifying credit in student loan forgiveness programs by reps only to find out later that they were given incorrect information. PSLF forgives your remaining balance, so this is a big deal.

So, you cannot trust loan servicer reps on this question.

What makes saying you're married but cannot reasonably access my spouse's income information fraud?

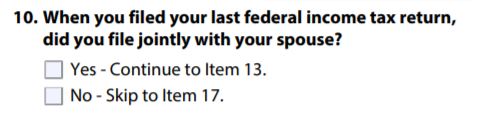

Generally, if you say you're married but cannot reasonably access my spouse's income information, you’re committing fraud. This is because it’s just not completely true. Here’s how the question appears on your IDR recertification request form:

When you say yes to this question, you’re technically at risk of committing a violation of this warning at the top of the form:

WARNING: Any person who knowingly makes a false statement or misrepresentation on this form or on any accompanying document is subject to penalties that may include fines, imprisonment, or both, under the U.S. Criminal Code and 20 U.S.C. 1097.

Fines, imprisonment, or both. That’s not something to mess around with because you want a different monthly payment amount. There are better ways to manage your federal student loan debt.

What is the risk the government will catch me or punish me?

In reality, auditing individual borrower information will not become popular until egregious cases of abuse leak out to the media. That will happen eventually, such as when the Government Accountability Office revealed some borrowers were misrepresenting their family size as having 93 people to avoid paying anything on their student loans.

Would the government go after you? Probably not, but they could. That principle leads everyone to try to be honest on their taxes: partly because it’s the right thing to do, and partly because they’re afraid of being caught.

Remember later on the IDR form, the government offers this out to you:

Again, if you answer no, then under PAYE, SAVE, or IBR you don’t need to include your spouse’s income at all in the calculation.

You will still have to provide it, but they won’t use it.

Here's one thing that’s mind-blowing. Some borrowers check they can’t access their spouse’s income even while filing a joint tax return.

That’s just pure foolishness. You’re saying on one form you can’t access your spouse’s tax information. But on another, you’re saying that you promise that all the income information you can see (including your spouse’s) is accurate. Those discrepancies would be the most obvious cases to prosecute if the government chose to do that.

Of course, we could eventually see reform of the system where spousal income becomes irrelevant to your individual student loan payments. It probably should be that way. But policymakers have long included a “marriage tax penalty”. This causes taxes to be higher on married couples than for individuals in many cases.

Get a plan so you don’t feel you have to commit fraud

You never need to fudge the numbers to pay as little as legally possible on your eligible loans. You just need to know and respect the rules.

Sometimes the Federal Student Aid site may be confusing and these rules and instructions are not very clear. This is the case, for instance, of community property states and providing acceptable alternative documentation of your income.

However, other loopholes, like filing taxes separately, are crystal clear.

You don’t need to come close to committing what could be fraud to get a great student loan plan. If you need one, just contact our experts.

We can discuss all options under IDR, deferment, forbearance, and refinancing so you know the best way forward for your situation. If you have private student loans from a lender, we can help you with those as well and discuss potential refinance opportunities.

What has your experience been saying you can’t access your spouse’s income? Who told you to do it? What is your reasoning? Would you do it if you could just file taxes separately instead? Comment below (and feel free to change your first name when posting).

Not sure what to do with your student loans?

Take our 11 question quiz to get a personalized recommendation for 2025 on whether you should pursue PSLF, IDR, or refinancing (including the one lender we think could give you the best rate).

Comments are closed.